Section World

Cooper presses Gulf partners to reopen Hormuz routes farmers need for fertiliser

Britain’s foreign secretary has tied Iran’s disruption of the strait to fertiliser reaching African fields and wider prosperity, while parallel reporting documents urea spikes, stuck cargoes, and UN hunger modelling that treat the next planting cycles as the clock that matters.

Foreign Secretary Yvette Cooper has placed fertiliser alongside energy when describing why a closed Strait of Hormuz hits countries that never dock a tanker in the Gulf. After a virtual summit that drew representatives from more than forty countries, she argued Iran had been able to “hijack” the shipping route and “hold the global economy hostage,” and she listed fertiliser supplies for farming in Africa among the lanes at risk—not only crude benchmarks traders watch by the minute.

The same public messaging stressed diplomatic and economic tools first: partners called for the immediate and unconditional reopening of the strait and respect for freedom of navigation, with London floating tighter United Nations pressure, possible sanctions if the passage stays blocked, and International Maritime Organisation work to get stranded hulls moving again. The United States did not take part in that particular diplomatic round, leaving European and Asian capitals to puzzle how far they can coordinate without being drawn into the wider US–Israel military campaign against Iran.

Cooper also framed the closure as a “direct threat to global prosperity,” language aimed at finance ministries as much as at public audiences. The point for food systems is more granular: nitrogen products move in huge volumes through Gulf export corridors; when those flows stall, cash-poor growers feel it before OECD shoppers notice empty shelves, because many smallholders buy sack-by-sack and can simply skip a planting if the maths fails.

Independent reporting from late April into May has documented urea jumping sharply, Qatari mega-plant cargoes halted, and analysts warning that even a reopened strait would leave queues and damaged plant capacity to clear—so the foreign-policy argument Cooper is making about urgency is running alongside commodity desks’ calendars, not against them.

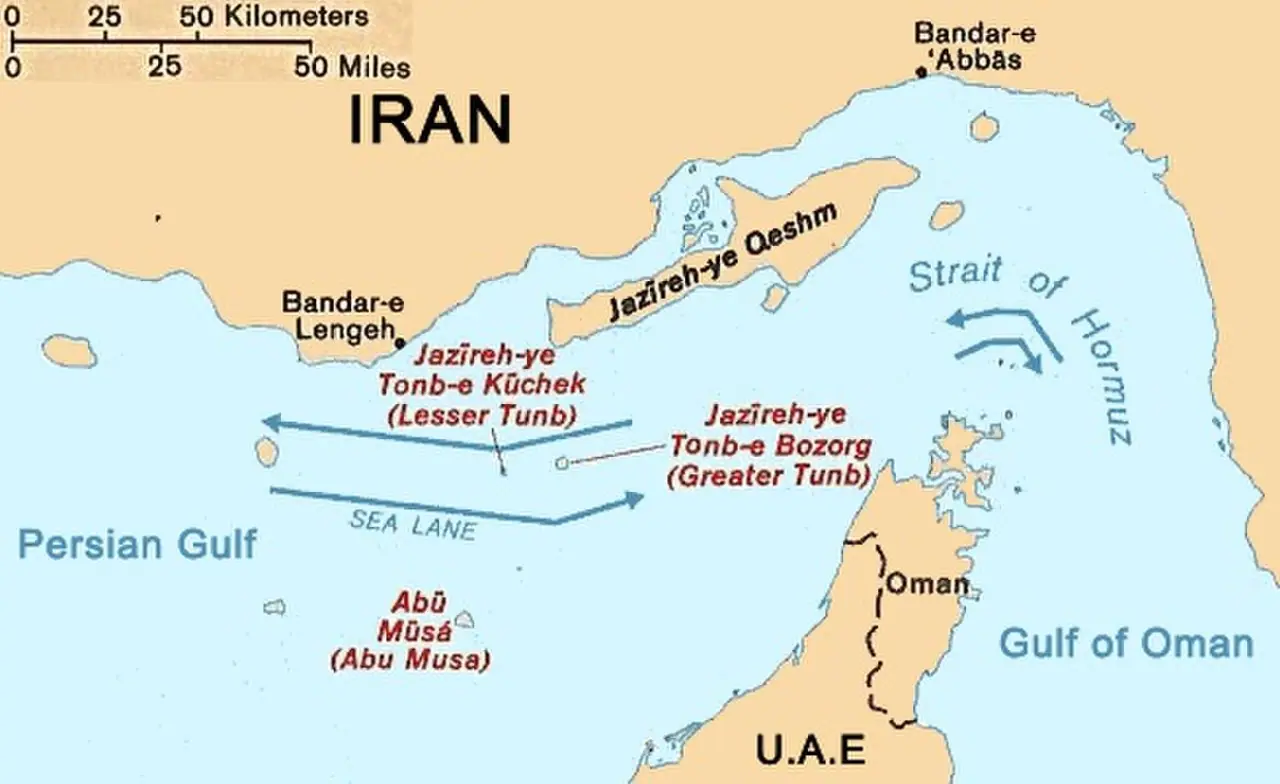

Hormuz closure and the fertiliser arithmetic

What disappears when the strait stops working

Roughly one-third of globally traded seaborne fertiliser has typically moved through Hormuz, according to trade reporting that tracked the channel before and after late-February strikes. When those flows stop, the world does not get a polite “pause” button on the crop calendar: nitrogen fertilisers such as urea are applied seasonally for many staples, so skipped applications show up months later in tonnage and quality, including protein levels in bread wheat.

Reuters-based analysis in late April cited traders estimating at least two million metric tons of lost urea production tied to conflict-linked shutdowns across several regions, with nearly one million tons already loaded but stuck in the Gulf—numbers that explain why clearing a maritime queue is treated as a weeks-long operational problem even after a ceasefire headline.

China’s parallel export gate

China is the world’s largest fertiliser producer; BBC reporting in early May noted it supplied about a quarter of global output last year and exported more than thirteen billion dollars’ worth, then tightened export curbs in March on several product lines while Hormuz risk was already feeding into gas-linked nitrogen costs. For Southeast Asia, the combination is brutal: Vietnam sourced more than half its first-quarter 2026 fertiliser imports from China by volume, the Philippines relies on China for about three-quarters of its fertiliser with almost no domestic fallback, and Thailand drew both Chinese supply and roughly a third of imports from the Gulf—so two separate corridors can fail at once.

That geometry is why diplomats’ warnings about prosperity are not abstract. When a Thai rice farmer tells reporters he will not plant because sack prices jumped from roughly eight hundred–nine hundred baht toward twelve hundred baht, the macro story lands in a single season’s lost hectares.

What the UK says it is trying before the shooting gets wider

Coalition scope and limits

The April talks Cooper summarised were billed as a first assembly point for countries willing to work on Gulf shipping security without folding every participant into the US–Israel combat narrative. French President Emmanuel Macron, speaking the same week from South Korea, called military reopening “unrealistic” and insisted a ceasefire and negotiations with Iran had to come first—an important fork for readers tracking whether London’s economic pressure talk can converge with Paris’s sequencing.

US President Donald Trump, meanwhile, publicly urged allies to “build up some delayed courage” and physically secure the route—a reminder that NATO and Asian partners face contradictory signals from Washington even when they agree on the economic harm of a long closure.

Sanctions, IMO logistics, and the fertiliser ask

Downing Street’s public line has been that British planners will weigh what might make the strait “accessible and safe after the fighting has stopped,” while Cooper’s immediate toolkit emphasis stayed on sanctions design, UN channels, and clearing trapped ships—steps that matter directly to fertiliser consignments that cannot afford indefinite demurrage arguments in secondary ports.

None of that guarantees quick relief: commodity analysts quoted in the same reporting window cautioned that fertiliser availability could stay tight for months after any political settlement because of plant damage, insurance clauses, and competition for alternative tonnes from the Americas and the Black Sea basin.

Hunger models, harvest calendars, and what to watch next

UN and analyst overlays

The UN World Food Programme, cited in BBC reporting on Asia’s food-security squeeze, estimated that combined fallout from the Middle East conflict could push about forty-five million additional people into acute hunger in 2026, with food insecurity in Asia and the Pacific projected to rise about twenty-four percent—the largest regional jump on their snapshot.

Those figures are models, not invoices, but they explain why foreign ministries are willing to sound dramatic about fertiliser at the same energy briefings: the humanitarian tail risk grows when growers from the Mekong to the Sahel defer planting because of input prices rather than because of lack of seed.

Hinge points for late 2026 and 2027

Agricultural councils are already trimming next-harvest forecasts; analysts quoted in commodity wire copy pointed to early signals such as expected double-digit wheat area cuts in Western Australia as farmers sidestep fertiliser-heavy, low-margin crops. If similar application cuts show up across major breadbaskets, 2027 balance sheets—not day-to-day diplomacy headlines—become the reckoning Cooper’s coalition rhetoric is trying to get ahead of.

Watch three lanes in parallel: whether Hormuz insurance and escort politics actually move stranded fertiliser hulls; whether Beijing loosens any export bans once domestic spring needs ease; and whether Gulf producers can restart ammonia and urea chains fast enough for a northern autumn top-dressing season that cannot be postponed with a press release.

Geography and themes

Related places and recurring themes for this story.

- United Kingdom

- Iran

- World

- Agriculture

Suggested reading

Other stories that pair well with this one—often from the same section or on overlapping themes.

Tehran floats Hormuz tolls on subsea internet cables as IRGC-tied media talk billions

Euronews and RFE/RL trace how Tasnim- and Fars-style outlets are packaging seabed leverage—transit fees, forced maintenance clauses, even cloud-giant localisation demands—while Mostafa Taheri, an Iranian parliamentary industries voice, throws around a headline revenue ceiling on the order of fifteen billion dollars annually that markets treated as rhetoric, not an invoice.

Tehran markets a ‘Hormuz Safe’ lane that settles marine cover in Bitcoin as war-risk premiums bite

Indian and trade-press explainers describe a new Iranian digital platform pitching blockchain-settled policies for commercial hulls threading the strait—complete with ministry talk of a ten-billion-dollar revenue ceiling—while compliance lawyers warn U.S. and EU persons that paying premiums into Iranian rails can still collide with sanctions law regardless of coin type.

Aftenposten Modi Cartoon Stirs Racism Row

Aftenposten ran Halleraker’s cartoon the same day as Rossavik’s Meninger column; Red MP Rana called it racist; political editor Alstadheim told Dagbladet the symbols backed Rossavik’s point and were not meant to demean.

Trump delays Iran strike after Gulf appeal

President Donald Trump said late on 18 May 2026 in Washington that he was postponing a U.S. military strike on Iran that had been scheduled for the following day after Qatar, Saudi Arabia, and the United Arab Emirates asked for time while diplomacy continued; he also told the armed forces to stay ready for a large-scale assault if talks fail.

Havana leans on self-defense law while rejecting US drone-strike talk as intervention pretext

President Miguel Díaz-Canel framed military deterrence as a lawful shield, not a war wish, after US-facing outlets amplified an Axios-style tally of imported drones; Washington’s January national-emergency declaration on Cuba still frames the island as an extraordinary threat.

Brazil’s TRF-1 faces a reckoning on whether Belo Sun’s Volta Grande gold license snaps back to freeze

After a single federal appellate judge revived the Canadian miner’s installation permit in February 2026, prosecutors appealed to the same court’s Sixth Panel—where the next collegiate ruling decides if the decade-old suspension logic from 2017 returns or the Pará project keeps rolling.

Brussels Brexit veterans say a UK return would mean normal EU membership, not the old carve-outs

Georg Riekeles and Sandro Gozi, among others, describe warmth toward a future application but zero appetite to recreate bespoke opt-outs; the Commission stays on this week’s brief—July summit prep—not hypothetical accession terms.

Kenya’s matatu shutdown over pump prices turns lethal as ministers report four dead

Interior Cabinet Secretary Kipchumba Murkomen’s tally—four killed, dozens hurt, and hundreds detained—lands atop a nationwide minibus strike that BBC reporting ties to another double-digit jump in regulated diesel and petrol caps.

Tarsus rampage leaves six dead and eight wounded as police scour Mersin for gunman

International outlets describe multiple shooting sites in southern Türkiye’s Tarsus district, a helicopter-backed manhunt, and a Cabinet-room toll readout from President Erdoğan while wire-sourced reporting sketches an alleged domestic-violence start and street-to-car attacks.

Hargeisa fills its 18 May squares with a post-recognition parade as Herzog seals the envoy link

Nairobi- and Tel Aviv–linked reporting described thousands in Hargeisa for the usual independence anniversary—this time under the glare of December 2025’s Israeli recognition—while President Isaac Herzog formally received Somaliland’s first ambassador in Jerusalem the same diplomatic window.

Keep exploring

Browse the full archive or return to the front page.

Sources and external links

Sources and filings our editors consulted to verify this story. External links open in a new tab.