Section Opinion

War has made the United States and Iran weaker—in different ways and on different clocks

Open conflict shrinks margin for both Washington and Tehran: budgets, energy markets, and domestic legitimacy absorb shocks that do not land symmetrically, even when each side still has lethal tools left.

Sustained United States–Iran fighting through spring 2026 has left both governments with less room to maneuver: fewer cheap diplomatic exits, thinner error margins, and markets that punish ambiguity at chokepoints faster than battle-damage summaries refresh. Weaker in this column means less slack, not equal hurt on a scoreboard—Washington and Tehran bleed on different calendars and with different toolkits.

The argument rests on two verified write-ups dated 3 April 2026 (strikes, diplomacy, Hormuz) and 28 April 2026 (U.S. macro and supply shocks); the live pages are listed under Sources. Every number that follows comes from that pair; the desk did not add independent battlefield or economic estimates. The tension running through both is that degradation on paper is not the same as a strait shippers and insurers will treat as normal, and that gap is where “mutual strain” becomes visible in payrolls and pump prices as well as in sortie counts.

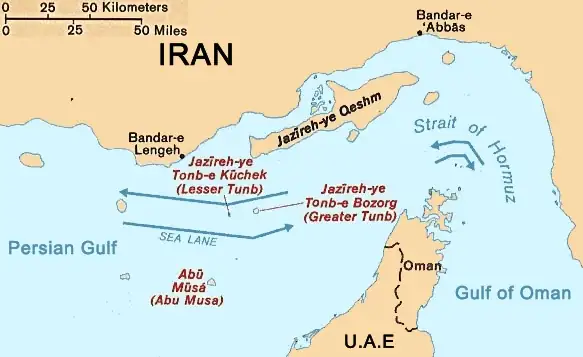

Military tally, Hormuz psychology, and why “degraded” is not “closed”

A 3 April accounting described a U.S. campaign aim of degrading Iran’s ability to project power—its navy, missile and drone stocks and production, and protection of nuclear infrastructure—while citing more than eleven thousand targets struck since this phase widened.

Iran’s larger navy was described as largely sunk; speedboats and dhows able to operate near the Strait of Hormuz were still called largely operational. Missile and drone forces were substantially degraded, yet the same analysis stressed that a handful of projectiles could still be enough to keep shippers and insurers wary—so Hormuz might fail the commercial definition of “open” even when headlines emphasize attrition. 28 February 2026 was marked as the hinge after which Hormuz was, in the sense that matters to schedules and insurance, no longer what it had been before.

Who pays at the pump when Hormuz carries mostly someone else’s barrels

The 3 April material noted that only about two percent of crude and condensate moving through Hormuz was described as bound for the United States, against roughly eighty to eighty-five percent for Asia and low single digits for Europe. That pattern does not spare American consumers from volatility: the same account cited U.S. average gasoline near four dollars per gallon to show pump prices still tracking global benchmarks despite limited direct barrel dependence.

It also cited external research estimating about 0.4 percentage points shaved off global real GDP growth in a baseline, a similar-sized hit to the United States, about 0.2 for China, and larger possible hits for some Asian economies excluding China. A further estimate attributed to that research tied the oil shock alone to slower U.S. payroll growth on the order of ten thousand jobs per month and a rise in unemployment of about 0.1 percentage points—small decimals that still read loudly in an election-cycle economy.

From helium to headline inflation: the late-April macro warning

The 3 April account traced Qatar’s role in helium—already tight in semiconductor steps—and disruption to coastal inventories, with downstream cost pressure in Asian fabrication and U.S. exposure on chips and data-center buildout if traffic stayed constrained.

The 28 April macro assessment treated Hormuz closure after the February widening of strikes as a global supply shock and warned total damage could exceed the scale of the 2022 European energy crisis. It noted a two-week ceasefire yet described traffic as still hardly matching what public reassurances had implied. It reported U.S. average gasoline above four dollars after a rise of more than one dollar and tied a jump in headline U.S. inflation from 2.4 percent in February to 3.3 percent in March to a large near-term gasoline swing in that accounting.

Hormuz, in the same material, was described as moving roughly one-fifth of world oil shipments alongside LNG, fertilizer, and helium—the bridge from a naval story to household ledgers.

Casualties and the politics of duration in Washington

The 3 April tally said thirteen American service members had been killed by Iranian fire since this phase began. One airman was listed missing in action after an F-15E went down over southwestern Iran; other casualties around the Gulf were tied to Iranian missile and drone strikes without a consolidated civilian ledger in that passage.

Aggregate U.S. power can coexist with a narrowing domestic margin: each death concentrates scrutiny of risk, rules of engagement, and how long leaders can defend continued exposure—pressure that does not replace carrier groups but can compress their freedom of action.

Uranium still inside Iran and diplomacy with almost no overlap

Roughly nine hundred seventy pounds of near-weapons-grade enriched uranium were reported still inside the country, possibly under rubble at Natanz or in Isfahan. Leadership losses among political and military elites were described as change at the top, not a claim of regime change.

The same analysis framed a fifteen-point U.S. proposal against a five-point Iranian response as having scant overlap. On one side sat demands to end Iran’s nuclear program, missile program, and proxy support; on the other, sanctions relief, guarantees against future U.S. and Israeli strikes, and sovereignty language tied to Hormuz. When the text of talks that thin overlaps with detonations offshore, both capitals risk looking tough at home while leaving observers unsure what, if anything, is still negotiable.

Asymmetry: different toolboxes, different definitions of “winning”

None of the above implies symmetry. Washington still draws on capital markets, alliance logistics, and reserve-currency plumbing at scales Tehran cannot mirror. Iran still leans on proxies, terrain, home-field familiarity, and pain tolerance shaped by decades of pressure.

The 3 April assessment echoed an asymmetric termination logic: sustaining a “not lose” posture versus needing a durable win. That is how many modern wars actually stop—messily, on more than one clock. Both sides can be weaker in slack without resembling each other in weakness.

What would change this assessment next

Those source pages describe partial ceasefires and ongoing strait friction; they do not deliver a final settlement as of their publication dates.

Hinges to watch: whether missile and air defense inventories reconstitute faster than diplomacy produces verifiable text; whether fissile material can be inspected rather than argued in the round; whether third-party efforts reopen traffic or only reroute risk; whether humanitarian and finance channels thicken or collapse. A durable ceasefire with verifiable limits on enrichment and missile testing, normalized chokepoint flows, and credible enforcement could rebuild margin for both societies. Proliferation cascades, neighboring collapse, or repeated strait closures would argue this column understates forward risk—not that either capital vanishes from the map.

Geography and themes

Related places and recurring themes for this story.

- United States

- Iran

- Middle East security

About the author

NewsTenet editorialEditorial board18 years' experience

Unsigned board line on standards, corrections framing, and when analysis should be labelled as opinion.

Focus areas

- Public policy

- Media literacy

- Economy and society

Suggested reading

Other stories that pair well with this one—often from the same section or on overlapping themes.

US–Iran war in the Middle East: who is involved, what each country is doing, and how they are affected

A widening U.S.–Iran war is fought with missiles and sanctions but lived through shipping insurance, food prices, refugee routes, and alliance politics from Manama to Mumbai—this is a full tour of the chessboard, not a scorecard of two capitals alone.

Revised Iranian proposal to end war shared with U.S., Pakistani source says

Prime Minister Shehbaz Sharif told a public event in Islamabad that Pakistan had received Iran’s written answer to Washington’s latest peace text, while Iranian state outlets framed the document around stopping the war and reopening shipping. Wire dispatches citing a Pakistani government official involved in mediation said the material was passed onward to the United States the same day.

Trump delays Iran strike after Gulf appeal

President Donald Trump said late on 18 May 2026 in Washington that he was postponing a U.S. military strike on Iran that had been scheduled for the following day after Qatar, Saudi Arabia, and the United Arab Emirates asked for time while diplomacy continued; he also told the armed forces to stay ready for a large-scale assault if talks fail.

Iran’s World Cup squad reaches Türkiye for camp while US entry papers stay unresolved

Wire and regional copy describe a May 18 departure toward Antalya for weeks of friendlies and logistics—still paired with federation warnings that American visas had not materialized and that FIFA was being asked to help secure guarantees before June fixtures in the United States.

Trump on Truth Social: Iran’s “clock is ticking,” move “FAST,” or “there won’t be anything left of them”

Agency-backed outlets reported on 17 May 2026 that U.S. President Donald Trump posted a capitalised ultimatum to Tehran on Truth Social amid fragile Gulf ceasefire diplomacy, quoting him verbatim as tying speed on a deal to survival while pairing the message with a reported call to Israeli Prime Minister Benjamin Netanyahu.

FBI maintains $200,000 reward for former US counterintelligence agent Monica Witt over Iran espionage charges

The former Air Force intelligence specialist remains a fugitive after defecting to Iran in 2013 and allegedly handing over highly classified national defense information.

Post analysis of satellite imagery ties Iranian strikes to damage or loss of at least 228 U.S. structures or pieces of equipment

A Washington Post investigation published in early May 2026 says it catalogued hangars, barracks, fuel sites, aircraft, and radar, communications, and air-defense assets hit across fifteen U.S. military locations in six Gulf and Levant partner states—arguing the tally dwarfs prior public U.S. disclosures while documenting how commercial imagery gaps and Iranian-published photos shaped what could be verified.

U.S. indicts Raúl Castro over 1996 plane shootdown

Federal prosecutors in Miami unsealed murder and conspiracy charges against the 94-year-old former Cuban leader for his alleged role in downing two civilian aircraft.

Barney Frank Dies at 86, LGBTQ Trailblazer

He came out in Congress in 1987, chaired Financial Services through the 2008 crash, and helped steer Dodd-Frank before retiring in 2013; his sister confirmed his death to NBC Boston.

Google CLI Links OpenClaw to Gmail Unsupported

Google's open-source Workspace CLI on GitHub links AI agents including OpenClaw to Gmail and Drive, but the company labels the project unsupported and warns workflows may break as APIs evolve.

Keep exploring

Browse the full archive or return to the front page.

Sources and external links

Sources and filings our editors consulted to verify this story. External links open in a new tab.

- Mission Accomplished? Taking Stock of the War in Iran (Council on Foreign Relations) (opens in a new tab)— Council on Foreign Relations

- What’s Next for the War in Iran? (Council on Foreign Relations) (opens in a new tab)— Council on Foreign Relations