Section World

US–Iran war in the Middle East: who is involved, what each country is doing, and how they are affected

A widening U.S.–Iran war is fought with missiles and sanctions but lived through shipping insurance, food prices, refugee routes, and alliance politics from Manama to Mumbai—this is a full tour of the chessboard, not a scorecard of two capitals alone.

Maps that shrink the 2026 crisis to arrows between Washington and Tehran capture the legal duel of two states yet underplay the operational mesh: maritime insurance, Gulf fiscal rents, Levant sovereignty stress, and Asian crude ledgers that can reprice inside a single session. Missiles and drones set one tempo; bills of lading, war-risk premiums, fuel piles for power stations, and refugee corridors set another in cities far from any declared front line.

What follows tracks who is doing what, where incentives diverge, and how costs propagate. Any aggregate strike tally, Hormuz traffic read, American casualty count, uranium-stockpile line, or GDP decimal tied to the war comes from April 2026 independent policy assessments listed under Sources—synthesis, not a live ordnance count. A companion NewsTenet Opinion piece on this site treats mutual strategic strain on different clocks.

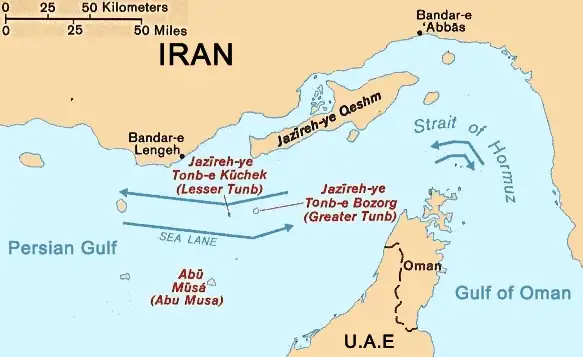

Why geography still bosses strategy

The Persian Gulf is shallow, hot, and crowded with offshore platforms, FPSOs, tanker lanes, and naval pickets. Hormuz is narrow enough that even modest missile or fast-boat harassment can change insurer behaviour faster than admiralties can publish reassurances. A parallel corridor runs through Bab el-Mandeb at the Yemen chokepoint: many Asia–Europe schedules can be forced into longer Cape routings when both passages look risky, burning fuel and time that show up later in retail prices and corporate margins.

That geography binds Iran to GCC neighbours whether they wish it or not. Riyadh and Abu Dhabi may see Tehran as a rival, but they still share gulf water physics with it. Oman sits on the Hormuz flank with a long Indian Ocean coast and a diplomatic tradition of talking to everyone; Kuwait and Bahrain sit almost inside the U.S.

Fifth Fleet footprint; Qatar anchors enormous LNG and industrial gas flows that matter to fertiliser and semiconductor steps thousands of miles away. None of those facts determines any government’s policy by itself, but together they explain why “non-belligerent” is not the same as “unaffected.”

Iran: defending a state while wielding a regional toolkit

Tehran enters this phase with a state interest in survival and a revolutionary tradition that treats export of influence as security in depth. Militarily, that has meant layering homeland air defences, ballistic and cruise missile inventories, drone swarms, and naval systems that can threaten Hormuz traffic even when blue-water capacity is attrited. Politically, it has meant relationships with non-state and state-aligned partners in Iraq, Syria, Lebanon, and Yemen—networks that extend deterrence and leverage beyond borders but also invite retaliation onto neighbours’ soil.

The April assessments summarised in metadata describe a U.S. campaign aimed at degrading Iran’s ability to project power—navy, missile and drone stocks and production, and protection of nuclear infrastructure—while citing more than eleven thousand targets struck since the phase widened. They characterise Iran’s larger navy as largely sunk but note speedboats and dhows that can still operate near Hormuz, and they stress that even a handful of remaining projectiles can keep shippers and insurers wary. That is the difference between a map that says “degraded” and a market that says “closed enough” to hurt.

On the nuclear file, the same synthesis reports roughly nine hundred seventy pounds of near-weapons-grade enriched uranium still inside the country, possibly under rubble at Natanz or in Isfahan—a sentence that captures how verification and targeting narratives can diverge from diplomatic text. Leadership losses among political and military elites are described as change at the top, not a claim of regime change; for ordinary Iranians, that still means inflation, rationing, blackouts, and currency pressure stacking atop sanctions architecture that predates this flare-up.

Diplomatically, the assessments sketch a fifteen-point U.S. proposal against a five-point Iranian response with little overlap: Washington emphasised ending Iran’s nuclear programme, missile programme, and proxy support; Tehran emphasised sanctions relief, guarantees against future U.S. and Israeli strikes, and sovereignty language tied to Hormuz. When talks that thin overlap with detonations offshore, both capitals can look domestically resolute while leaving outsiders unsure what, if anything, remains negotiable.

United States: expeditionary power meets voter-facing economics

Washington’s role is the one superpower expeditionary package: carrier air wings, long-range precision, intelligence fusion, alliance logistics, and the diplomatic muscle to demand overflight, basing, and sanctions alignment from partners. The April synthesis ties that role to an attrition strategy—degrading Iranian tools rather than narrating a simple regime-change invasion—while still acknowledging that duration and domestic politics can compress freedom of action as casualties accumulate.

That political channel matters because the same assessments tally thirteen American service members killed by Iranian fire since the phase began, list one airman missing in action after an F-15E went down over southwestern Iran, and note additional casualties around the Gulf tied to missile and drone strikes without a consolidated civilian ledger in that passage. In a democracy, small absolute numbers can carry large strategic weight: each death sharpens questions about rules of engagement, exit criteria, and whether Congress and the public accept the theory of victory being offered.

Economically, Hormuz is where local war meets global price discovery. The April material notes that only about two percent of crude and condensate moving through Hormuz was described as bound for the United States, against roughly eighty to eighty-five percent for Asia and low single digits for Europe—yet U.S. average gasoline was still cited near four dollars per gallon, illustrating how American consumers can absorb volatility through benchmark markets even when direct barrel dependence is small. The same research summary estimated about 0.4 percentage points shaved off global real GDP growth in a baseline, a similar-sized hit to the United States, about 0.2 for China, and larger possible hits for some Asian economies excluding China, with further estimates tying the oil shock alone to slower U.S. payroll growth on the order of ten thousand jobs per month and a rise in unemployment of about 0.1 percentage points—decimals that read loudly in an election-cycle economy.

A companion macro assessment in the same source cluster treated Hormuz disruption after a late-February 2026 widening of strikes as a global supply shock and warned total damage could exceed the scale of the 2022 European energy crisis; it reported U.S. average gasoline above four dollars after a rise of more than one dollar and tied a jump in headline U.S. inflation from 2.4 percent in February to 3.3 percent in March to a large near-term gasoline swing in that accounting. It also described Hormuz as moving roughly one-fifth of world oil shipments alongside LNG, fertiliser, and helium—the bridge from a naval story to household ledgers and data-centre build-out anxieties when traffic remains constrained.

Israel: a technologically deep actor on an overloaded frontier

Israel’s role overlaps U.S. aims but is not identical to them. Jerusalem has long treated Iranian nuclear latency, precision missile programmes, and proxy encirclement as existential file folders; its toolkit—airstrikes, covert disruption, missile defences, and intelligence—often intersects American timing even when both governments insist on sovereign decision-making. In practice, that intersection can speed escalation when both capitals believe a window is closing, or it can create friction when Washington wants de-escalation optics while Israel still sees proliferation risk as intolerable.

Effects cascade through mobilisation economics, tourism cancellations, northern border vigilance, Gaza-linked security burdens, and diplomatic positioning with Arab states that have moved toward normalisation but still carry public opinion sensitive to Palestinian suffering. Gulf capitals watch Israeli actions as signals about how long the U.S. will tolerate high-tempo operations that can pull Iranian retaliation eastward into Arab skies.

Gulf Arab monarchies: rents, bases, and the mediation premium

Saudi Arabia and the United Arab Emirates anchor GCC wealth and defence modernisation: huge sovereign wealth pools, gigaproject spending timelines, and imported air-defence architectures that assume stable energy exports. Kuwait and Qatar combine enormous per-capita income with foreign-policy styles that lean harder on mediation and media diplomacy. Bahrain hosts the U.S.

Fifth Fleet headquarters; Oman trades access for autonomy and often carries messages others cannot.

Their shared effect channel is strait risk: insurance, freight, and demurrage can spike faster than spot crude mean-reverts, tightening fiscal space for states whose budgets still move with oil even when they diversify. Qatar-linked LNG and helium nodes matter because modern industry treats industrial gases as quietly critical inputs; disruption narratives can move semiconductor planning before tanker counts change. Public posture must triangulate Iranian proximity, street sympathy, U.S. security guarantees, and Asian customer relationships—four audiences that rarely want the same sentence from a foreign ministry on the same day.

Iraq, Syria, and Lebanon: where sovereignty meets proxy geometry

Iraq sits on the fault line between U.S. troop presence, Iran-linked Popular Mobilisation politics, Kurdish autonomy questions, and parliamentary factions that can rhetorically oppose Washington while institutions still depend on dollar flows and electricity imports. That is not hypocrisy so much as structural trap: asserting sovereignty without triggering a larger war the Iraqi state cannot survive.

Syria adds a collapsed service grid and sanctions complexity; any Israeli air campaign that reaches Iranian assets on Syrian soil renews debates about international law, humanitarian access, and Russian air-defence legacy systems. Lebanon carries Hezbollah-linked deterrence and a banking crisis that predates the current Gulf fight; missile exchanges that touch Beirut’s hinterland can collapse what little fiscal margin remains and reignite refugee politics in Jordan and Turkey.

The common effect is humanitarian density: displacement, cholera risk when water treatment fails, currency collapse that makes imported food unpayable, and youth unemployment that militias monetise. Neighbouring mediators watch these arcs because refugee shocks and radicalisation risk scale nonlinearly with duration—a lesson Europe learned painfully in the 2010s even when the Mediterranean was the busier corridor.

Yemen and the Red Sea: a second maritime axis

Yemen-based factions aligned with Iranian interests have used anti-ship weapons to reshape Red Sea traffic, raising the economic cost of support for Israel and complicating U.S. logistics. Bab el-Mandeb is not interchangeable with Hormuz, but for Asia–Europe container lines it can be the margin that decides whether schedules detour around Africa.

Humanitarian funding for Yemen itself remains chronically underfed; a widening Gulf war can push aid further down donor priority lists even as needs rise. Piracy risk narratives can also resurface when coastguards are overstretched—another hidden tax on trade.

Egypt, Jordan, and Türkiye: buffers that still have to balance books

Egypt monetises Suez tolls, tourism, and remittances; risk premia that deter tankers can also deter container optimism, while Gaza-adjacent instability keeps military readiness expensive. Jordan imports most of its energy and water ideas; refugee hosting already shapes domestic politics, and any Lebanese or Syrian spillover tightens housing and wage competition.

Türkiye mixes NATO membership with Black Sea trade, Syrian buffer zones, and energy deals that let it talk to Moscow and Gulf capitals simultaneously. Ankara can offer mediation rhetoric with real corridors, but inflation-sensitive voters feel imported energy shocks quickly—so foreign policy ambition and household pain move on linked clocks.

Asian importers: the demand basin that actually moves Hormuz barrels

China, India, Japan, and South Korea are not combatants in the U.S.–Iran core fight, yet they are the principal consumers of the risk it generates because they are the principal consumers of the barrels that still move—or stop—through Hormuz. The April analyses cited in metadata portrayed the majority share of Hormuz crude and condensate as Asia-bound, with Europe taking a smaller slice and only a sliver tied directly to U.S. refiners.

Effects propagate through electricity tariffs, fertiliser costs for rice and wheat farmers, petrochemical margins, and currency defences. India and Pakistan face current-account stress when oil whipsaws; Japan and Korea worry about LNG co-loading with crude insurance clauses; China can deploy price controls and reserve releases, but those tools have administrative costs and distortions that show up later in debt and efficiency metrics.

Russia, China, and the European Union: leverage without carrier decks

Moscow and Beijing typically supply diplomatic off-ramps, commodity partnerships, and United Nations framing that competes with Western narratives while avoiding direct combat entanglement. Russia can market itself as a swing seller when Gulf barrels look risky, but must manage sanctions enforcement risk on its own exports. China can rhetorically champion sovereignty while privately urging stability because Belt and Road financiers hate insurance spikes.

Brussels coordinates sanctions, humanitarian funding, and energy security lessons from the 2022 Ukraine shock; EU gas systems are less Russia-dependent than at that war’s start but remain price-takers on LNG margins. European NATO members simultaneously manage U.S. troop posture debates and Middle Eastern freedom-of-navigation statements—two files that can collide when publics want both defence solidarity and de-escalation.

Feedback loops that make endings messy

Wars like this stop less often with a single capitulation than with stacked partial outcomes: a ceasefire line here, a strait traffic regime there, a sanctions carve-out for humanitarian finance, and a nuclear inspection formula that neither side loves but both can sell at home. Military maps lag market maps; market maps lag humanitarian counts when access is contested.

Watch for second-order shocks—whether dollar funding tightens for fragile importers while oil stays elevated, whether humanitarian corridors shrink faster than donors refill them, or whether insurer retreat lingers after kinetic tempo falls. Those channels do not replace the Gulf–Levant core; they explain how a regional war can read as global within a week.

Ceasefire mechanics, inspection regimes for fissile material, and verified strait traffic statistics will move household ledgers more than a single day’s sortie list; those are the signals that should update this explainer next.

Geography and themes

Related places and recurring themes for this story.

- Iran

- United States

- Israel

- Middle East security

Suggested reading

Other stories that pair well with this one—often from the same section or on overlapping themes.

Trump on Truth Social: Iran’s “clock is ticking,” move “FAST,” or “there won’t be anything left of them”

Agency-backed outlets reported on 17 May 2026 that U.S. President Donald Trump posted a capitalised ultimatum to Tehran on Truth Social amid fragile Gulf ceasefire diplomacy, quoting him verbatim as tying speed on a deal to survival while pairing the message with a reported call to Israeli Prime Minister Benjamin Netanyahu.

Revised Iranian proposal to end war shared with U.S., Pakistani source says

Prime Minister Shehbaz Sharif told a public event in Islamabad that Pakistan had received Iran’s written answer to Washington’s latest peace text, while Iranian state outlets framed the document around stopping the war and reopening shipping. Wire dispatches citing a Pakistani government official involved in mediation said the material was passed onward to the United States the same day.

War has made the United States and Iran weaker—in different ways and on different clocks

Open conflict shrinks margin for both Washington and Tehran: budgets, energy markets, and domestic legitimacy absorb shocks that do not land symmetrically, even when each side still has lethal tools left.

Trump delays Iran strike after Gulf appeal

President Donald Trump said late on 18 May 2026 in Washington that he was postponing a U.S. military strike on Iran that had been scheduled for the following day after Qatar, Saudi Arabia, and the United Arab Emirates asked for time while diplomacy continued; he also told the armed forces to stay ready for a large-scale assault if talks fail.

Israel says it killed Hamas Gaza military chief Izz al-Din al-Haddad; Hamas official confirms death to Reuters

Prime Minister Benjamin Netanyahu and Defence Minister Israel Katz said Israeli forces targeted Izz al-Din al-Haddad in Gaza City on 15 May 2026, describing him as a surviving architect of the 7 October 2023 attacks; international wires then reported a senior Hamas official confirming his death while medics counted at least seven fatalities in related strikes and families prepared a Saturday funeral.

FBI maintains $200,000 reward for former US counterintelligence agent Monica Witt over Iran espionage charges

The former Air Force intelligence specialist remains a fugitive after defecting to Iran in 2013 and allegedly handing over highly classified national defense information.

Post analysis of satellite imagery ties Iranian strikes to damage or loss of at least 228 U.S. structures or pieces of equipment

A Washington Post investigation published in early May 2026 says it catalogued hangars, barracks, fuel sites, aircraft, and radar, communications, and air-defense assets hit across fifteen U.S. military locations in six Gulf and Levant partner states—arguing the tally dwarfs prior public U.S. disclosures while documenting how commercial imagery gaps and Iranian-published photos shaped what could be verified.

Iran’s World Cup squad reaches Türkiye for camp while US entry papers stay unresolved

Wire and regional copy describe a May 18 departure toward Antalya for weeks of friendlies and logistics—still paired with federation warnings that American visas had not materialized and that FIFA was being asked to help secure guarantees before June fixtures in the United States.

U.S. indicts Raúl Castro over 1996 plane shootdown

Federal prosecutors in Miami unsealed murder and conspiracy charges against the 94-year-old former Cuban leader for his alleged role in downing two civilian aircraft.

Cooper presses Gulf partners to reopen Hormuz routes farmers need for fertiliser

Britain’s foreign secretary has tied Iran’s disruption of the strait to fertiliser reaching African fields and wider prosperity, while parallel reporting documents urea spikes, stuck cargoes, and UN hunger modelling that treat the next planting cycles as the clock that matters.

Keep exploring

Browse the full archive or return to the front page.

Sources and external links

Sources and filings our editors consulted to verify this story. External links open in a new tab.

- What’s next for the war in Iran? (Council on Foreign Relations) (opens in a new tab)— Council on Foreign Relations

- The U.S. economy and the Iran war shock (Council on Foreign Relations) (opens in a new tab)— Council on Foreign Relations